Telehealth is no longer a niche service. It’s become the dominant distribution channel for prescription access in DTC healthcare. As the DTC healthcare marketing landscape shifts toward performance-based acquisition, the affiliate channel has become one of the most underleveraged tools in the stack.

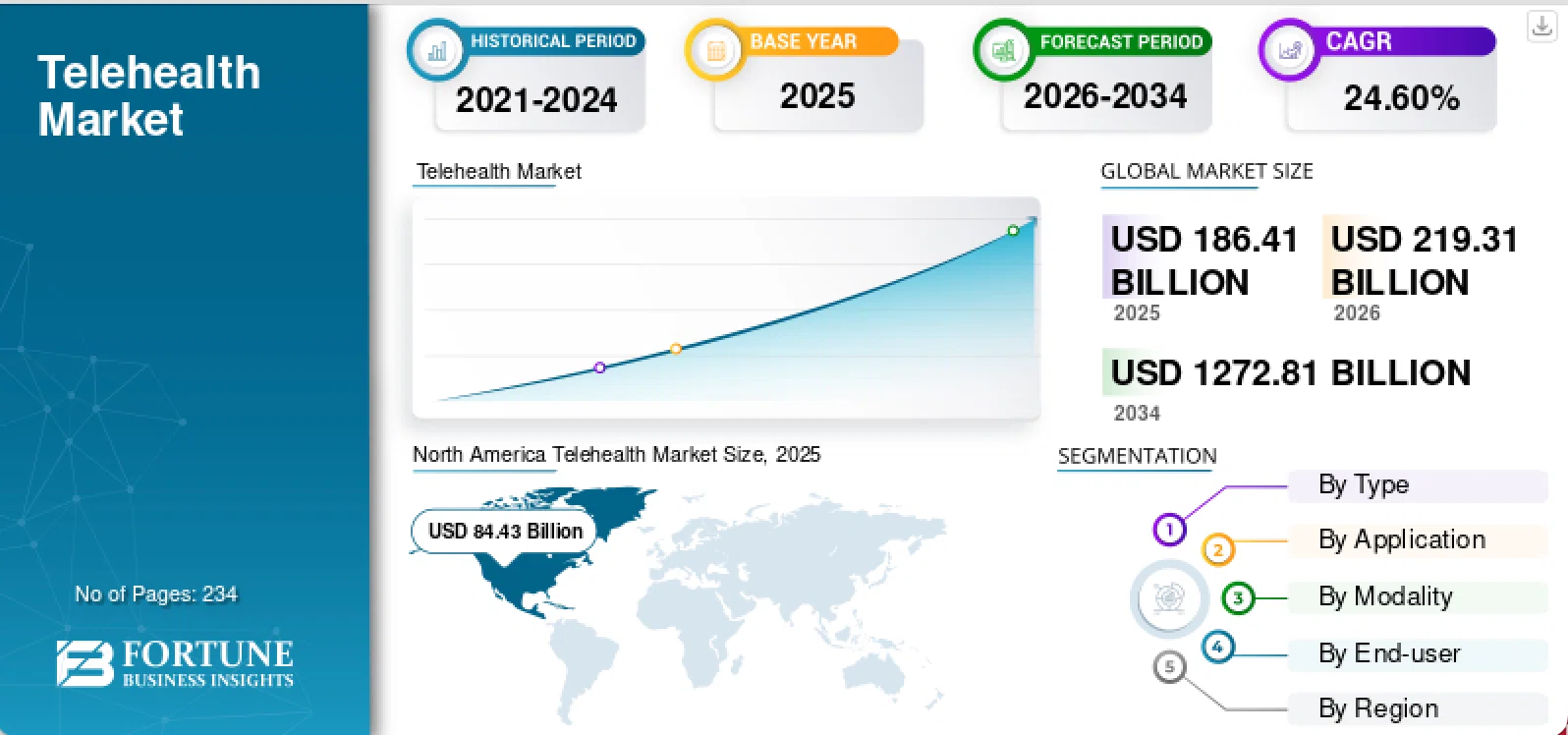

According to Fortune Business Insights, the telehealth market is expanding at 22.9% annually and is projected to reach $791 billion by 2032. Companies like Ro, Nurx, Hims & Hers, and newer entrants are acquiring patients at scale, building vertically integrated platforms designed to maximize customer lifetime value—not maximize transaction volume.

The global telehealth market is projected to grow from $219.31 billion in 2026 to $1,272.81 billion by 2034. (Source: Fortune Business Insights)

The same principle applies to an affiliate program strategy. My team internally analyzed four years of affiliate performance data across 10 DTC healthcare brands to see whether the data supports what we’ve been seeing on the ground. We built this analysis specifically to answer a question we kept hearing from DTC healthcare brands: why is our paid social CAC rising while this channel sits underallocated?

Over 11,000 partner-level records. $167 million in cumulative spend. $132 million in tracked revenue. These programs deployed $84 million in 2025 alone, with 2026 trending significantly higher. This is among the more comprehensive performance datasets we’ve seen in this vertical.

The data revealed 77% of affiliate budget is going to partner types returning less than 1x ROAS, while just 6% is generating the strongest returns. This concentration problem isn’t a small optimization opportunity. It’s evidence that most brands are misallocating budget at the portfolio level—and the gap between performance and spend is wider than it’s ever been.

The regulatory environment is creating new economics. The creator ecosystem is delivering returns that outperform most paid channels. AI-driven patient discovery is opening a front door that barely existed two years ago. These shifts are structural, not cyclical. The brands that recognize what the affiliate channel has become—and reallocate accordingly—will be the hardest to catch.

Healthcare affiliate performance and ROI benchmarks

Transaction-based brands in our portfolio deliver a median 4.4x return on ad spend (ROAS) — results that rival paid social and search benchmarks of 2–4x ROAS across the same sector. Three brands in the dataset consistently return above 6x, a threshold that, for a telehealth brand retaining patients at $80/month, represents an acquisition cost that pays back within the first 60 days of a subscription.

The highest-performing partner type outperforms every benchmark in the portfolio. Creator partnerships generated $12 million in revenue on $1 million in spend: 11.8x ROAS at a $15 cost per acquisition. For context, that’s three times the return of the best-performing paid channel in the same dataset — and it’s performance-based. Every dollar is tied to a verified conversion, not an impression.

The affiliate channel isn’t a secondary acquisition lever. For brands willing to move budget toward the partner types that actually deliver, it’s a primary performance channel. The gap between what the top performers are earning and what the average brand is achieving isn’t a skill gap. It’s an allocation gap — and it’s wider than most programs realize.

Which affiliate partner types deliver the highest returns

Two partner types in our data return above 1x ROAS. Together, they account for 6% of total spend.

| Partner Type | ROAS | Share of Budget | Best Fit For |

| Creator partnerships | 11.8x | ~3% | Telehealth subscriptions, trust-based Rx acquisition |

| General affiliate networks | 1.4x | ~3% | OTC volume, broad market reach |

| Content & editorial partners | 0.85x | ~45% | Awareness; limited direct conversion |

| Cashback & loyalty programs | 0.52x | ~32% | One-time OTC purchases; high churn risk for subscriptions |

Seventy-seven percent of affiliate budget is going to partner types that return less than a dollar for every dollar invested. Six percent is generating the strongest returns.

Rebalancing even a fraction of that 77% toward creator partnerships, niche health publishers, and condition-specific communities—the partner types where clinical credibility and audience trust are built in—can materially shift portfolio performance.

These aren’t channels brands buy your way into with higher CPMs. They’re relationships built on relevance. That’s what makes them hard to replicate and why the brands building them now will be protected from the brands scrambling to build them later.

Why healthcare sub-vertical segmentation changes everything

The dispersion problem

DTC healthcare isn’t monolithic. The same affiliate channel serves three fundamentally different business models simultaneously, and blending them into a single portfolio view is where most programs lose visibility.

Across our portfolio, CPA ranges from $13 to $68 among transaction-based brands. Revenue-per-action ranges from $41 to $183. That dispersion isn’t noise. It reflects Rx, OTC, and telehealth operating under completely different acquisition economics, and it punishes any program that treats them the same way.

A $68 CPA is disqualifying for a supplement brand and a strong investment for a telehealth subscription where patient lifetime value exceeds $500 in year one. A creator partnership that performs for a wellness product may require an entirely different compliance structure for an Rx brand. A cashback partner that drives OTC volume will attract deal-seekers who churn immediately from a subscription.

What segmentation actually reveals

The brands extracting the most value manage Rx, OTC, and telehealth as separate businesses: separate partner strategies, separate ROAS targets, separate measurement windows.

What they find when they do is performance that looked mediocre in the blend reveals real pockets of strength. One brand in our portfolio carried an “average” 2.1x blended ROAS—a number that would prompt a budget review in most programs. Segmented, it contained a 4.8x creator channel buried beneath content partnerships that only made sense for the OTC side of the business. The creator channel wasn’t underperforming. It was invisible.

Blended reporting hides this. Segmented reporting reveals it, and changes every subsequent allocation decision.

What’s driving the shift in DTC healthcare affiliate economics

Four structural forces are converging on DTC healthcare affiliate simultaneously. Each one independently favors reallocation toward creator partnerships and performance-based channels. Together, they make the case for moving now rather than later.

Creator maturation

Healthcare-specific creators have built real audience trust over the past 18 months—and the data confirms they outperform every other partner type in the portfolio. That trust is becoming measurable in ways that go beyond engagement metrics.

According to Datos and SparkToro’s Q4 2025 State of Search report, NIH ranked among the top destinations after an AI search, but didn’t appear among the top 15 destinations following a traditional Google search. Meaning patients using AI tools to research health decisions are actively seeking clinical authority to verify what they find. The creators and niche publishers producing that clinical content are the ones getting cited. The brands that have built compliant programs around them are building the entry to patient acquisition before it becomes obvious that’s what they’re building.

SparkToro Co-founder & CEO Rand Fishkin notes that the most revealing domains in AI search data are those that don’t show up in traditional top search destinations. [source: Datos and SparkToro’s Q4 2025 State of Search report]

The FDA’s extension of advertising scrutiny to influencer content further raises the compliance bar. Brands still building medical-legal review workflows later will pay more, wait longer, and enter a creator market where the best relationships are already committed. The compliance moat is already forming.

Regulatory tailwinds

The Inflation Reduction Act’s first negotiated drug prices are live. The Consolidated Appropriations Act of 2026, signed into law February 3, requires pharmacy benefit managers to delink compensation from Medicare Part D drug rebates and move to flat administrative fees.

These shifts create margin room that didn’t exist before implementation—margin brands can now direct toward acquisition channels tied to verified outcomes rather than impression volume. The economics of going direct to the patient have rarely been more favorable, and performance-based affiliate is the channel best positioned to capture that margin advantage.

Patient LTV

DTC healthcare subscriptions retain at significantly higher rates than traditional retail DTC—platforms in our portfolio report 80%+ retention at three months. The brands measuring affiliate performance in patient lifetime value rather than single-transaction ROAS are making different capital allocation decisions as a result.

A $68 acquisition retaining at $80/month for 18 months returns $1,440 in revenue. A $13 acquisition that churns in 60 days returns $160. The channel math looks entirely different when programs measure the right thing, and the brands that have already rebuilt their measurement frameworks around LTV are making better partner selection decisions every quarter they run.

Competition

Eli Lilly, Pfizer, Novo Nordisk, and Bristol Myers Squibb all have live DTC offerings. These entrants bring significant acquisition budgets. As they move into creator partnerships and niche publisher relationships, CPAs for health-credentialed creators will rise, and inventory will tighten.

The brands already in those relationships will have the pricing advantage. The brands still building them will be paying pharmaceutical-company rates to get there, for partners that are already committed elsewhere.

How brands reallocate DTC healthcare performance marketing budget

Start with the audit

Brands can’t reallocate what you can’t see. Before moving budget, map your current spend distribution by partner type—creators, content and editorial, cashback and loyalty, general networks—and by sub-vertical. Most programs discover the 77% problem only when they look at partner type and sub-vertical simultaneously. The audit is what makes the reallocation intentional rather than reactive.

Shift the partner mix

Begin moving budget toward the partner types the data says are working: creator partnerships, niche health publishers, condition-specific communities. Not all at once, but with a specific reallocation target and a quarterly review cadence.. A 10% shift from cashback and loyalty toward creator partnerships is enough to move blended ROAS materially while the new relationships develop. Set a reallocation threshold, track it quarterly, and adjust based on what the segmented data reveals.

Separate the measurement

Brands like Ro—where a single patient can move through telehealth consultation, Rx fulfillment, and OTC wellness products within the same platform—are running three different acquisition businesses through one affiliate program. Each sub-vertical has different partner economics, different LTV profiles, and different compliance requirements. Blending them into a single ROAS target produces a number that accurately describes none of them.

Give each sub-vertical its own partner strategy, ROAS targets, and measurement window. A content partner that looks mediocre in the blended portfolio may be the highest-performing driver of OTC awareness when measured on its own.

A creator partnership that looks expensive at first transaction may be the highest-LTV channel in the telehealth sub-vertical, where the patient who converts through a trusted creator retains at a materially higher rate than one who converts through a cashback link. The brands doing this are finding performance they already had — it was just invisible in the blend.

Change what you measure

Single-transaction ROAS is the wrong standard for a subscription business. Programs that build cohort-level LTV into affiliate reporting can track customer value at 90, 180, and 365 days from acquisition. That $68/$13 math from above applies here directly. A $13 acquisition that churns in 60 days returns $160. The partner selection decisions look completely different when you’re measuring the right thing. The brands that have rebuilt their measurement frameworks around LTV are compounding their allocation advantage every quarter. The brands still optimizing for first-transaction ROAS are making the same misallocation decision repeatedly without knowing it.

Frequently asked questions about DTC healthcare affiliate

In DTC healthcare performance marketing, creator partnerships in 2026 the highest-performing partner type in DTC healthcare affiliate, delivering 11.8x ROAS at a $15 cost per acquisition. General affiliate networks return 1.4x ROAS. In contrast, content and editorial partnerships average 0.85x ROAS, and cashback/loyalty programs return 0.52x ROAS. The performance gap between creator partnerships and traditional affiliate channels is significant and continues to widen as healthcare-specific creators build audience trust and establish clinical credibility.

Performance variation in healthcare affiliate reflects fundamentally different business models operating simultaneously. Telehealth subscriptions with patient lifetime values exceeding $500 can support a $68 patient acquisition cost. OTC and supplement brands may find that same CPA unprofitable due to lower lifetime value. Rx brands face different compliance requirements than OTC partners. Cashback partners attract deal-seekers who churn quickly from subscription services but drive volume for one-time purchases. Blended portfolio reporting hides these differences. Segmented reporting by business type (Rx, OTC, telehealth) reveals hidden pockets of strength and guides more precise budget allocation.

For DTC healthcare brands looking to reduce dependence on paid social, creator-driven affiliate delivers 11.8x ROAS in DTC healthcare, compared to paid social and search benchmarks of 2–4x ROAS in the same sector. Beyond the return differential, creator affiliate is performance-based, meaning you pay only for conversions, not impressions. This eliminates the risk of spend on non-converting traffic. Additionally, creator partnerships build brand awareness and trust alongside direct response—a benefit paid channels struggle to deliver simultaneously.

Patient lifetime value (LTV) fundamentally changes how you evaluate affiliate partner profitability. A brand with telehealth subscriptions retaining at 80% at three months with $80/month recurring revenue can justify a higher cost per acquisition than a brand with lower retention or lower recurring value. The same $68 cost per acquisition is disqualifying for some brands and highly profitable for others, depending on customer LTV. Measuring only single-transaction ROAS masks this reality. Cohort-level LTV tracking—measuring customer value at 90, 180, and 365 days—reveals which partners actually drive profitable growth long-term.

Start with an audit of current spend distribution by partner type. Most DTC healthcare brands allocate 77% of affiliate budget to partner types returning less than 1x ROAS, while just 6% of spend drives the strongest returns. Begin reallocation with intention: shift budget from underperforming channels (cashback, content partners) toward high-performing channels (creator partnerships, niche publishers, condition-specific communities). Segment by sub-vertical (Rx, OTC, telehealth) to reveal which partners perform best for each business model. Implement partner-level performance tracking and LTV measurement to guide ongoing allocation decisions.

Healthcare performance marketing in 2026: the reallocation that changes the CAC math

The brands that recognize what this channel has become—and invest accordingly—will be the hardest to catch.

The data doesn’t suggest optimization. It demands reallocation, and the structure for doing it is visible now. It demands reallocation. The winners in DTC healthcare affiliate over the next 12–24 months won’t be the brands with the biggest affiliate budgets. They’ll be the ones spending in the right places.

The structure is visible now. The competitive advantage goes to the brands that act on it.