In Thailand, 9 of the top 10 TikTok creators by revenue aren’t influencers in the traditional sense. They’re Key Opinion Sellers, or creators built for conversion, not just reach. That distinction is playing out across the region.

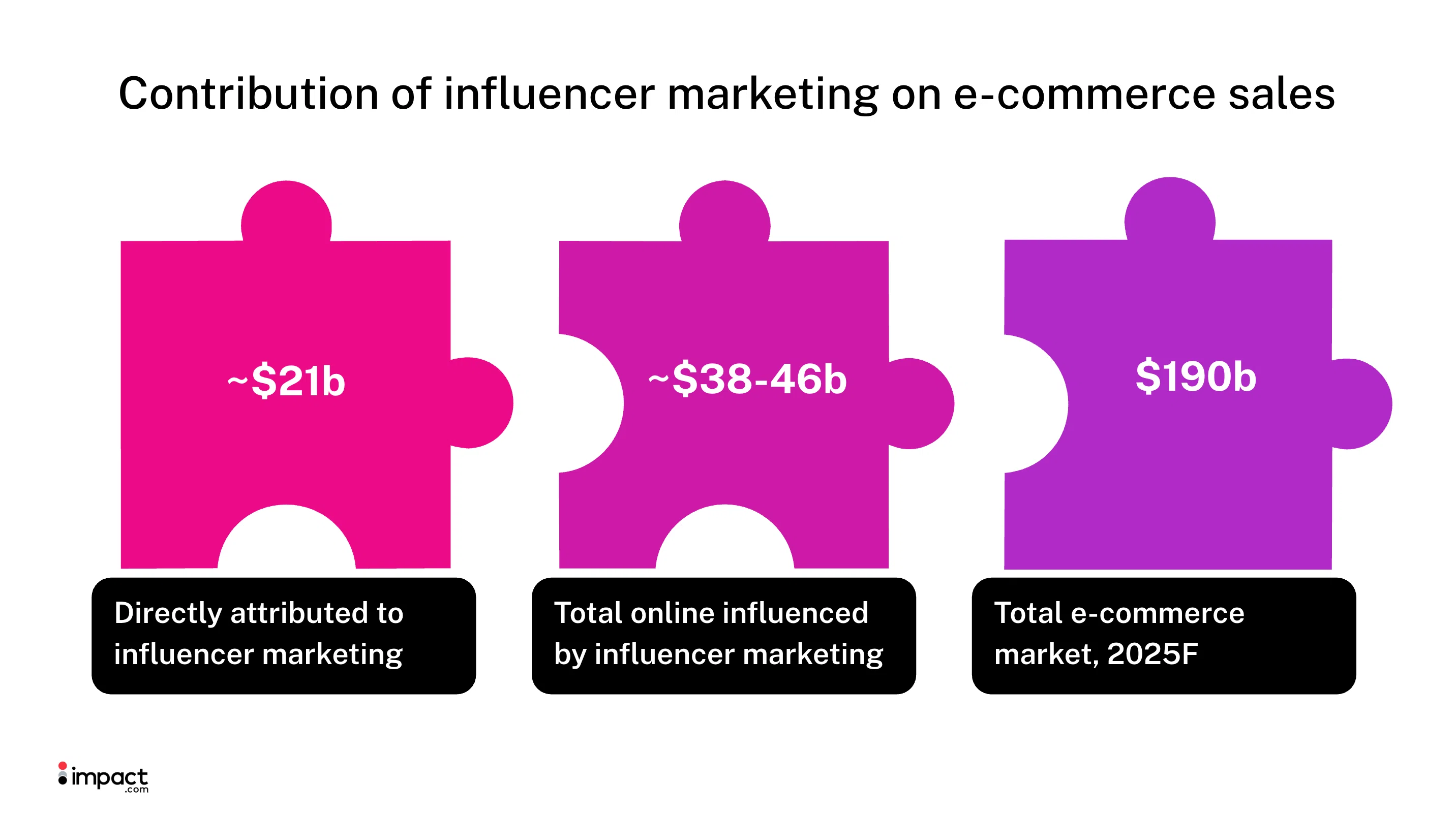

Influencer marketing in Southeast Asia now drives up to $46 billion in ecommerce sales, with $21 billion directly attributable to creator campaigns. Yet consumer trust is declining across every tier—from celebrities down to nano influencers.

The two things happening at once tell the story. Volume is up. Trust is fragmenting. That combination means reach alone no longer moves the needle the way it used to—and the brands seeing sustained growth know it.

The data points to a new era of how brands work with influencers. At $46 billion, creator marketing is already a commerce channel. The question is whether your program is built to operate like one.

All data in this article is sourced from the Cube × impact.com Southeast Asia Influencer Marketing Report 2025, based on a survey of 2,400 consumers and interviews with 30 industry stakeholders across Singapore, Malaysia, Indonesia, Thailand, Vietnam, and the Philippines, unless otherwise noted.

Why influencer marketing in Southeast Asia requires a strategic shift

The old model was simple: Find influencers with big followings. Pay them for posts. Hope the exposure translates to sales.

That approach worked when social platforms were newer and audiences were less skeptical. Today’s savvy consumers are more selective about the recommendations they act on. They want authenticity, relevance, and proof that a creator genuinely uses what they promote.

At the same time, platforms have built closed-loop commerce ecosystems. TikTok Shop, Shopee, and Lazada now offer end-to-end attribution, allowing you to trace a sale from content to checkout.

This changes the economics entirely. Instead of paying for impressions, you can pay for results.

5 trends shaping influencer marketing across Southeast Asia in 2026

Trend 1. Consumer trust is harder to capture than ever

Consumer trust is showing signs of strain across every influencer tier.

The sharpest pullback came at the top, with celebrities and mega influencers seeing the largest declines. The trust gap between tiers is narrowing, but not because smaller creators are gaining ground—trust in larger influencers is eroding faster.

Audiences are more aware of paid partnerships. They can spot scripted content. And they’re less willing to trust recommendations that don’t feel genuine.

| Influencer tier | Positive impact on purchasing decisions | YoY change |

| Mega influencers (>1M followers) | 59% | -7% |

| Celebrities | 55% | -8% |

| Macro influencers (100K-1M) | 54% | -5% |

| Micro influencers (10K-100K) | 44% | -3% |

| Nano influencers (1K-10K) | 34% | -4% |

When a decline in trust affects every tier, no category can carry reach and conversion alone. This suggests that creator diversification is no longer optional.

As influencer marketing matures into a structured commerce channel, concentrating investment in a single tier introduces potential imbalances. Programs built around one tier can limit your ability to balance reach, credibility, and attributable sales within the same system.

What you can do: Build strategic creator ecosystems

- Stop chasing follower counts. Look for creators who demonstrate product expertise and consistent engagement with their audience.

- Build a diversified creator portfolio across tiers. Use larger creators to drive awareness and narrative, and performance-driven creators to drive attributable sales.

- Invest in long-term influencer partnerships that give trust time to build. A creator who promotes your product once is a contractor—a creator who talks about your brand repeatedly becomes an advocate.

Trend 2. Influencer content converts when you use attributable formats

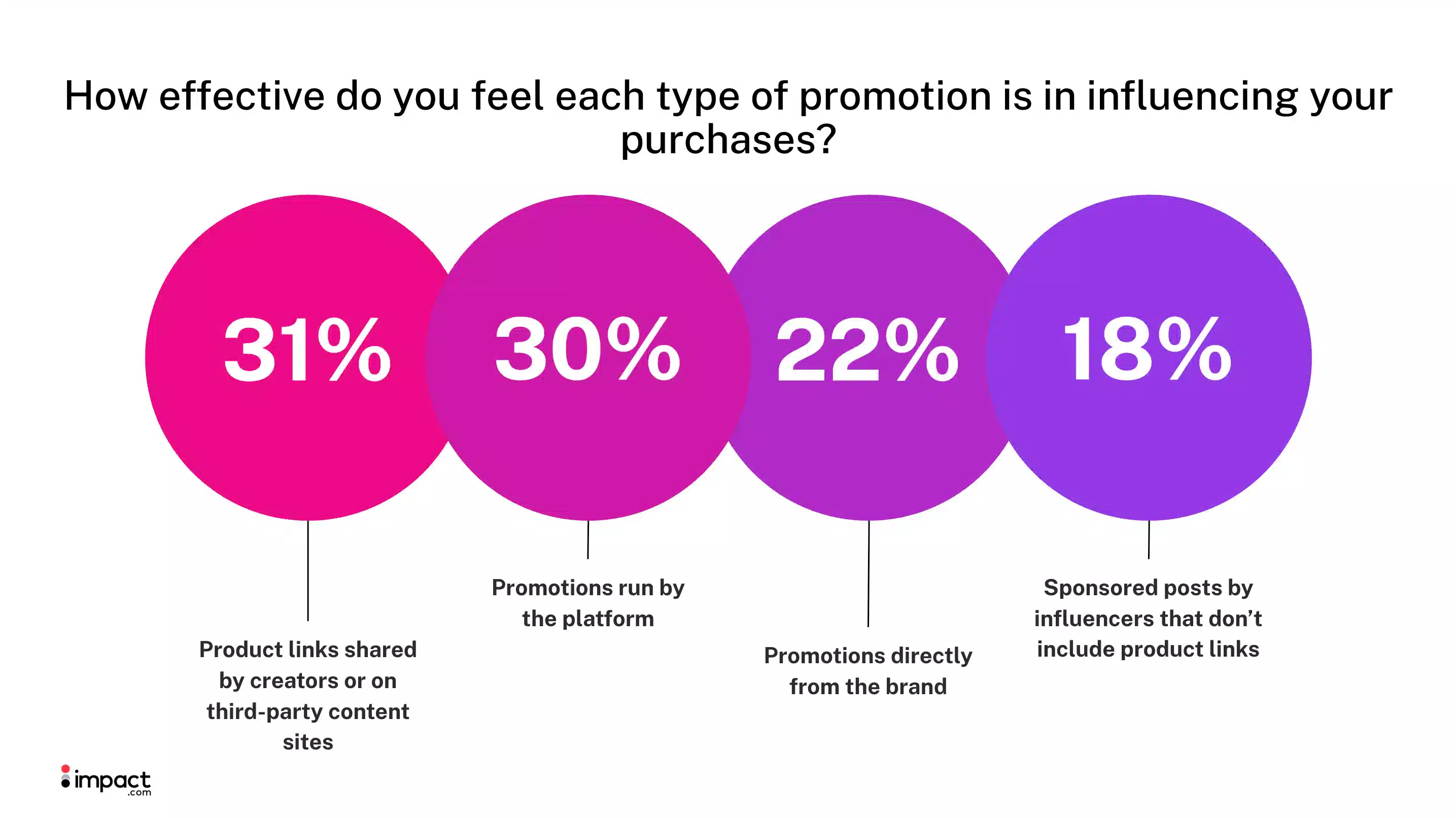

Creator content influences 59% of consumers to buy, but format determines how persuasive it is.

The data showed a clear hierarchy:

- Influencer content with product links were the most convincing out of all promotional methods (31%)

- Influencer content without a clickable path to purchase was less persuasive (18%)

This aligns with how consumers now shop. They discover products through creator content, then expect to buy immediately within the same platform.

That expectation—discover and buy in the same moment—is where most sponsored content fails. When a creator recommends a product but there’s no link to act on, you’ve created friction where intent is highest. A shoppable post removes that gap. A non-clickable sponsored post turns a purchase moment into a search exercise.

What you can do: Align content formats to funnel intent

- Match your creator content formats to what you’re trying to achieve. Use non-clickable content sparingly for top-of-funnel awareness. For consideration and conversion, prioritize shoppable posts, affiliate links, and live commerce.

- Track success by attributable actions, not impressions.

Trend 3. Consumers expect to shop through affiliate links

Affiliate-driven purchasing is now mainstream across Southeast Asia. The report found that 83% of consumers have purchased products through affiliate links on brand websites or ecommerce platforms.

What’s more, 60% of consumers view affiliate links positively. They see them as trust signals, convenience tools, or ways to support creators they like. Only 8% expressed negative sentiment.

At this level of adoption, affiliate links are familiar territory. Shoppers expect a clear path to purchase when a creator recommends a product—and campaigns that rely solely on non-trackable sponsorships are misaligned with how consumers convert.

While affiliate purchasing is common across the region, some markets use it more heavily than others.

| Affiliate purchase penetration by country | Share of consumers |

| Indonesia | 90% |

| Vietnam | 90% |

| Malaysia | 86% |

| Thailand | 83% |

| Philippines | 80% |

| Singapore | 69% |

Certain categories lend themselves more naturally to affiliate-driven purchasing. The dominance of beauty, fashion, and groceries isn’t accidental. Creator endorsement carries disproportionate weight in these verticals, and their high purchase frequency turns a single affiliate link into a repeat revenue driver instead of a one-off sale.

For brands in these sectors, affiliate-linked creator content is now table stakes. For others, the opportunity is clear: category-adjacent audiences are already primed to buy where trust is established.

| Top affiliate purchase categories | Share of affiliate buyers |

| Beauty and personal care | 62% |

| Fashion | 54% |

| Groceries | 36% |

What you can do: Make it easy for creators to share direct product links

- Treat affiliate links as a default commerce pathway. Build your creator programs with affiliate mechanics from the start.

- Give influencers easy access to trackable links, and make the landing page experience clear, fast, and reliable.

- Transparency matters, but don’t overcorrect. Audiences already expect creators to earn from recommendations.

Trend 4. Creator types and compensation models drive different outcomes

Not all creators do the same thing, and how you pay them determines what they do for you. As Southeast Asia’s influencer economy matures, understanding creator types and incentives is essential for building influencer programs that actually work.

There are three dominant creator models operating in the region today, each with different motivations and benefits for brands.

| Influencer type | Role | Audience size | Strength | Compensation model |

| Key Opinion Leaders (KOLs) | Shape public opinion and build brand credibility | Large followings | Storytelling, lifestyle influence, brand equity | Prefer fixed fees and sponsored deals |

| Key Opinion Consumers (KOCs) | Share authentic product reviews | Small to mid-sized audiences | Relatability and trust within niche communities | Often motivated by product experience, smaller fees, or light incentives |

| Key Opinion Sellers (KOS) | Drive immediate sales and conversions | Varies (often strong live audiences) | High-energy selling, urgency, real-time interaction | Thrive on commission and platform performance incentives |

A KOL on a commission structure will underperform because you’ve removed the conditions they need to do their job. The same applies in reverse: a KOS on a fixed fee has no skin in the game. Creator type and compensation model have to work together, or one undermines the other.

Fixed fees remain the most widely used model across Southeast Asia, but momentum is shifting toward commission and hybrid structures as brands demand clearer ROI accountability. The ecosystem is moving towards performance.

| Compensation type | Description | Brand adoption | Outlook |

| Fixed engagement fees | Cash fees for specific deliverables, can include brand usage rights and campaign expenses | High | Stable – Fixed fees remain the most widely used payment model |

| Sales commission fees | Commissions on sales, typically for a specific ecommerce channel. | Growing | Positive – Brands are shifting toward commission-based payment models to drive efficiency |

| Product sponsorship / payment-in-kind | Influencers, especially those with smaller followings, often receive free products as sole remuneration for their work | Moderate | Stable – Sponsorship of free products for review is table-stakes for influencer marketing |

| Hybrid | Combines fixed engagement fees and sales commission. | Increasing | Positive – Hybrid models offer balance between guaranteed fees and performance incentives |

Incentives shape behavior. Commissions favor conversion-led creators, while fixed fees favor influence-led roles. The wrong incentive can weaken results or skew them.

For many brands, the real risk isn’t choosing the wrong creator—it’s misapplying incentives. Brands that match creator type to incentive will build more durable programs.

What you can do: Match creator type to business objective and compensation model

- Avoid evaluating KOLs and KOS using the same framework. Build separate engagement and measurement models for influence-led creators (brand building) versus conversion-led creators (sales generation).

- Use compensation to shape the behavior you want. If you want brand storytelling, pay fixed fees. If you want sales velocity, pay commission. If you want both, use hybrid structures with clear expectations for each component.

- Don’t mix compensation models without defining success for each. A KOL on a pure commission structure is likely to underperform—not because they’re ineffective, but because you’ve applied the wrong incentive to the wrong archetype.

Trend 5. Creator affiliates are now core commerce infrastructure—and platform economics determine how they operate)

Creator affiliates aren’t a side tactic anymore. Influencer marketing currently drives 20-24% of Southeast Asia’s total ecommerce sales, including $21 billion in directly trackable affiliate and performance revenue. By 2030, that’s forecast to reach 22-26% of a $375 billion market, equivalent to $82-97 billion annually.

What changes the nature of the opportunity is measurability. Today, about 11% of ecommerce sales are trackable to influencer activity. By 2030, that figure is expected to rise to 13-17% as closed-loop platforms expand and attribution improves.

When you can track the entire journey, the creator relationship stops being transactional. You’re building ongoing partnerships where creators have a direct stake in performance.

But that infrastructure doesn’t operate in a vacuum. Platform commission rates, attribution rules, and ecosystem openness increasingly shape where creators focus and how brands should structure deals.

Marketplace commission rates on TikTok Shop, Shopee, and Lazada range from 4-13% depending on category. Beauty, fashion, and electronics pay the highest rates, which naturally pushes creator activity toward those sectors. Over time, this raises payout expectations and reduces pricing flexibility for brands competing in those spaces.

Attribution rules add another layer:

- TikTok Shop offers the most affiliate-friendly model, paying on both direct sales and indirect sales when a buyer clicks and purchases something else

- Shopee and Lazada are more restrictive, limiting indirect attribution to platform-funded products

- Brand.com programs typically run 1-12% but give brands control of the customer relationship and more flexibility to customize structures

The platform you choose isn’t just a distribution play. It determines what you can measure, what creators are incentivized to do, and how much of the customer relationship you actually own.

Not all platforms are equal partners in that infrastructure.

| TikTok Shop | Shopee & Lazada | Brand.com | |

| Commission rate range | 4-13% | 4-13% | 1-12% |

| Attribution model | Direct + indirect sales | Direct sales only (indirect limited to platform-funded products) | Customizable |

| Brand ownership of customer | Platform owns relationship | Platform owns relationship | Brand owns relationship |

| Flexibility | Low—locked into ecosystem | Low—locked into ecosystem | High—you control the structure |

| Best for | Conversion velocity, affiliate scale | Marketplace reach | Long-term customer value, data ownership |

What you can do: Build affiliate infrastructure with platform economics in mind

- Design influencer programs with affiliate mechanics built in from the start. Align incentives around sales outcomes while preserving creative freedom.

- Evaluate platforms based on attribution clarity and incentive alignment, not just audience size. The platform with the largest user base isn’t always the one that best serves your business model.

- Weigh closed-platform efficiency against brand ownership. TikTok Shop offers tracking advantages but locks you into their ecosystem. Brand.com programs give you more control and customer data but require more infrastructure investment.

- Bring your influencer, affiliate, and ecommerce teams together around shared KPIs. The separation between those functions creates attribution gaps that let value leak.

- Plan for scale, not campaign-by-campaign execution. Brands that capture the most value build an always-on creator roster with consistent incentives, performance benchmarks, and revenue-based reinvestment rules.

AI, automation, and the next phase of influencer-led commerce

One more trend deserves attention: artificial intelligence.

The report projects that by 2027, up to 50% of digital content could be AI-generated. Tools like Google’s Veo 3 and ByteDance’s Seedance 1.0 already produce photorealistic video from text prompts, complete with cinematic camera movement and consistent characters.

This creates both opportunity and risk. You can scale content production dramatically. But audiences may grow skeptical of AI-generated material, especially where trust matters most.

The report anticipates several responses:

- Famous creators may license their name, face, and voice to brands, enabling AI to generate content on their behalf

- Platforms may offer built-in persona licensing tools

- Audiences may demand “human-certified” or “authentically made” labels to signal real human creation

Industry interviews reveal skepticism about AI’s ability to replicate genuine human connection. But the technology is advancing fast. The creators and brands who figure out how to blend automation with authenticity will have an edge.

That edge has a specific shape. If half of digital content is AI-generated by 2027, credibility will be the scarcest thing in the content ecosystem. The trust data in this report is already showing strain across every influencer tier, and that’s before AI floods the feed.

A creator with a genuine audience relationship and a track record of honest recommendations becomes more valuable in that environment. The commerce infrastructure argument and the AI argument point to the same conclusion: human credibility is the asset worth building programs around.

The consumer shift has already happened in Southeast Asia. Has your program caught up?

Eighty-three percent of consumers have purchased through affiliate links. Influencer channels already drive up to $46 billion in regional ecommerce. Trust is declining across every creator tier even as volume grows.

That combination means the brands still running influencer marketing as a brand awareness investment are funding infrastructure that the market has already moved past.

Creator affiliates, closed-loop attribution, and performance-based compensation are how ecommerce operates in this region now. The programs built around those mechanics are compounding.

The question for 2026 is whether your program is built to operate like a commerce channel or is it still optimized for reach?

Frequently asked questions

Influencer marketing in Southeast Asia connects brands with creators who have built trust with specific audiences. This activity drives $38 to $46 billion in regional ecommerce sales because consumers increasingly discover and purchase products through creator recommendations.

Influencer-led sales are concentrated on TikTok Shop, Shopee, and Lazada, where marketplace commission rates range from 4–13% and affiliate attribution is built in. Influencer marketing already contributes 20–24% of total ecommerce sales in the region, largely through these closed-loop platforms. Broader social platforms like YouTube and Facebook drive discovery, but commerce infrastructure lives on marketplaces.

KOLs Key Opinion Leaders (KOLs) are traditional influencers focused on brand building, storytelling, and audience engagement. Key Opinion Sellers (KOS) are performance-first creators who drive immediate sales through livestreams and shoppable content. KOLs build credibility. KOS drive conversions. In Thailand, 9 of the top 10 TikTok creators by revenue are KOS.

Marketplace platforms offer 4-13% commission rates depending on category. Beauty typically pays highest at 10-13%. Fashion averages 8-10%. Electronics sits at 4-9%. Brand.com programs usually offer 1-12%.

Only 18% of consumers rate sponsored posts without product links as effective. Product links shared by creators (31%) and platform-run promotions (30%) perform significantly better. If conversion is your goal, include a clickable path to purchase.

83% of consumers surveyed have purchased through affiliate links. Penetration is highest in Indonesia and Vietnam (90% each), followed by Malaysia (86%), Thailand (83%), Philippines (80%), and Singapore (69%).

By 2027, up to 50% of digital content may be AI-generated. This could lead to creator licensing, platform-based avatar tools, and growing demand for “human-certified” content labels. Most brands remain cautious, but the technology is advancing quickly.